Let's talk about financial literacy in India.

According to a survey conducted by the Global Financial Literacy Excellence Center, less than 25% of the adult Indian population is financially literate!

This means that if you were to sample a group of 100 Indian working adults, less than 25 of them would know how to handle their finances or increase their wealth through assets!

Let's see the stats of some other countries.

Denmark and Sweden are the leading countries with 71% literacy rates, followed by Canada, Israel, Germany, and the UK with 65-68% while the US has 57%. Moreover, according to S&P’s Global FinLit Survey, India has one of the lowest financial literacy rates!!!

But what is Financial Literacy??

According to the definition, Financial Literacy is the knowledge and understanding of key financial skills, from budgeting and saving to investing and retirement planning, and the ability to put them to use in your life. Simply put, Financial Literacy refers to the knowledge and behaviors that help an individual make accurate decisions regarding their money.

From here, we have another word - Investing.

Investing is the practice of channeling money into financial schemes or assets with the expectation of profit. In simpler terms, investing is using your money to make more money!! There are 5 different asset classes one can invest in:-

- Cash= The cash class has 3-4 different types of investment options. Some of the most popular ones are Savings bank accounts and Liquid Funds. Hard cash is also a part of this asset class. This asset class has options that are very liquid and short-term in nature with a maturity of 1 year or less. This class is almost risk-free with almost no potential for growth.

- Fixed Income/Debt= This is by far one of the most popular asset classes in India. This class consists of instruments like bonds, loans, and money market securities, which give regular payments to their investors. People normally invest their money into these assets and claim regular payments (monthly or quarterly) until these assets mature. It is a fairly safe asset class to invest in but has low growth potential.

- Real Estate= This asset class refers to the investment in physical properties like apartments, flats, land plots, commercial offices, industrial properties, and others. One can buy these properties to rent them out for monthly payments and hold them until the value of the property surges. Although there is potential for capital appreciation, there are risks of market fluctuations and added costs like maintenance.

- Commodities= This class invests in assets like wheat, oil, copper, gold, silver, and several other commodities. The main reason to invest in this class is to diversify one’s investments. Moreover, this class grows with inflation, so your earnings increase. However, there is higher volatility here and the assets are very reactive to global developments.

- Equity= Also called stocks, this is one of the most misunderstood asset classes. Stocks allow one to own a stake in a company and avail the benefit of corporate actions like stock/cash dividends or capital appreciation. Although this is the riskiest out of all classes, it is also the class with the highest growth potential.

But why should anyone invest??

Some people wish to have more money today, some wish for a sumptuous retirement fund while some wish for more money to spend on trips or luxuries!

Irrespective of an individual’s motive, investing can help them earn more money by putting their stagnant money to work. Moreover, an added benefit of investing is that it helps individuals stay ahead of inflation.

Inflation is the general increase in the prices of goods and services which causes a reduction in the purchasing power of money.

Let’s take an example to understand the concept. Suppose a person has Rs.100 to spend and with that, he chooses to buy 10 pens for Rs.10 each. However, companies cannot maintain the same price with the rising costs of raw materials, higher energy prices, and growing labor costs.

So, considering an average inflation rate of 6.5% per annum, the price per pen jumped to Rs 10.65, resulting in a total expense of Rs 106.50. Due to this increase, the individual will not be able to buy 10 pens anymore.

This phenomenon is seen in all products across the world, essentials and luxuries. Therefore, every individual will be required to register a growth of more than the inflation rate every year. With banks paying less than 4% & 9% interest every year, a savings or FD is certainly not good enough.

Now, let’s see the life of an average Indian man.

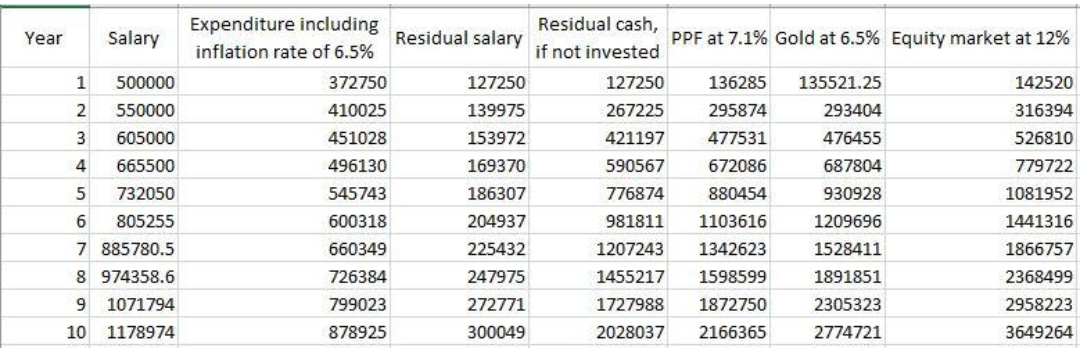

The man earns Rs. 5,00,000 in year 1 and gets a salary increment of 10% every year for 10 years and then retires. His annual expenditure is 70% of his salary which increases every year by the inflation rate of 6.5%.

In the table, we see that the man saves close to Rs 20.3 lakhs if he chooses not to spend/invest his surplus. However, at the end of 10 years, inflation won’t stop growing as prices will continue to increase. Therefore, the purchasing power of the man’s residual cash will also decline, making the money less valuable.

The man would run out of money in 5 years if he did not invest the money into an investment scheme that generates returns more than the inflation rate.

Moreover, if he pumps all his residual money into a savings account, the 4% interest earned will not be higher than the inflation rate, making it a poor investment choice.

However, if he chooses to invest in financial assets, then he would have Rs. 21.67 lakhs from PPFs (the annual investment is restricted to Rs 1,50,000 from the third year), Rs. 27.74 lakhs if invested in gold, and Rs. 36.5 lakhs from the equity markets which is 1.8 times the value of the residual cash!!

Hence, we can see why investing in equities is so important!

1,499

1,499